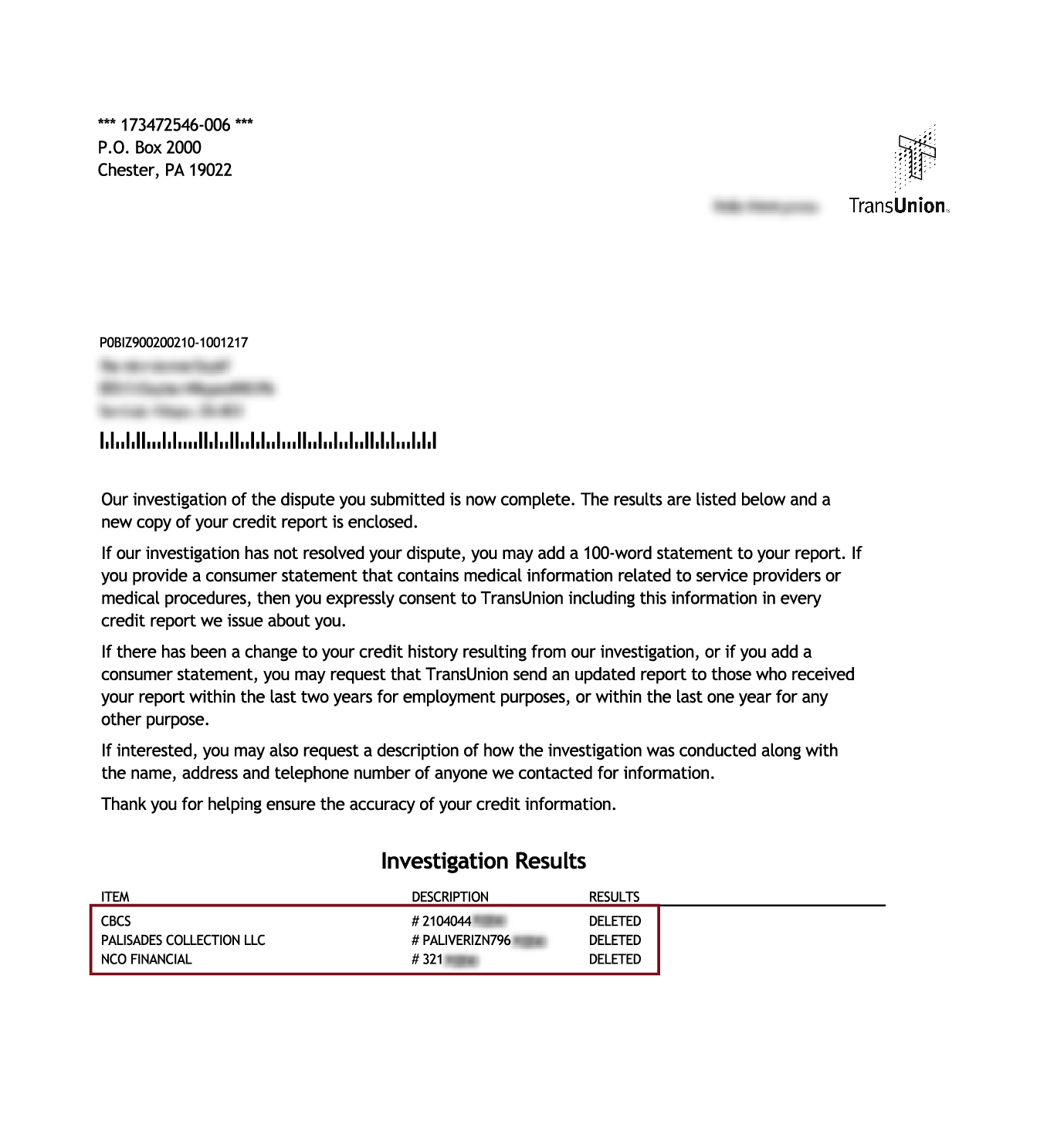

Image source: https://aaacreditguide.com/app/uploads/2017/05/collections01.jpg

Second off, and before we do anything else we need to be clear about what is meant by the term, Collection Agency, and it is basically one of three things:

1) A company that has been assigned a debt, for collection.

2) A company that has purchased a debt, for collection.

3) A lawyer who has been hired to collect a debt.

And the third most important think to be clear about, is which kind of debts can you settle and they are things like:

a) medical bills,

b) credit cards,

c) personal loans,

d) department store cards,

e) student loans,

f) bounced checks.

The reason that all the above are good candidates for debt settlement, is that they are all unsecured debts, but don't expect to settle a mortgage or an auto loan, because the lender can repossess them, and therefore doesn't need to come to any kind of arrangement with you.

Assuming that the person that contacted you is a debt collector, that he or she represents a Collection Agency, and that the debt is an unsecured one, we will now look at two more things that must be verified before you even think of settling the debt.

You must first validate the debt, which in essence means that you make sure that the company or person requesting payment, has been authorized to collect the debt, and is who they say they are, and there are many articles on the web explaining how to do this.

The second must do thing, is to check is whether or not the debt is within or outside of the statute of limitations, and if the debt is outside of the statute of limitations then tell the collector that you know that it is, and demand that he stop harassing you.

Don't Be Confused

Just because a debt has been removed from your credit report, doesn't mean that you don't owe the money, and there is often some confusion about this.

In almost every case, a bad debt and all related comments must by law be removed from your credit report after seven years, and if it's still there then contact the credit agency and they will remove it.

This law applies to credit agencies though, and should not be confused with the statute of limitations on debts, so be sure to check the laws for your state very carefully.

Some Important Dos And Don'ts

1) Try to handle all correspondence by mail so there's a paper trail, and use registered mail, receipt requested, and make sure you keep a copy.

2) If you do have to speak on the phone, then make a note of the date and time, the person that you spoke to, and what was discussed.

3) Always believe that the agency will accept less than they say they will.

4) Stay calm and remind yourself that the collection agency wants to strike a deal and that time is on your side, and never forget that the more time that passes, the less you'll have to pay.

5) Never ever say that you need to settle the debt.

6) Never accept their first or even second offers.

7) If they really press hard, then threaten them with bankruptcy, and if they believe you, then they'll always settle quickly, and for less.

8) A debt collection agency can sue you, but it's a long process, costs money and it's the last thing that that the agency wants to do, so don't panic.

So How Much Should You Offer?

The agency most likely paid between five and seven cents on the dollar if the debt is a recent one, and as little two cents if the debt is an old one, and if it's very old, and we're talking several years, then the debt might have been bought for as little as one cent on the dollar.

To keep the math simple, let's say that the debt is $2,000 and it's a recent one, then the agency probably paid around 120 dollars (6%) for it, and if it's very old then as little as twenty dollars, so I would suggest offering them 20% of the original amount if it's a recent debt, which would be 400 dollars, and expect them to settle for around 500 dollars and offer them 250 dollars (10-15%) if it's an old debt.

If you're contacted by a second debt collection agency, then be sure that they have the right to collect the debt, and if they do then you can pretty safely assume that they paid even less for the debt than the first agency, so offer them even less.

Be Very Wary Of Penalties And Padding

It's very common for debt collection agencies to add on huge amounts of interest based on the original debt, and that's called usury, and it's illegal in every state, so remember that the agency bought the debt for a few cents on the dollar, and that's what they can charge you interest on.